Why Goldman Sachs Shareholders Should Vote FOR Proposal #7

Goldman Sachs has spent over $55 million on lobbying since 2010, yet shareholders are not told how those funds are used. Here's why they should vote FOR proposal #7 on April 29.

Goldman Sachs has spent over $55 million on lobbying since 2010, yet shareholders are not told how those funds are used. Here's why they should vote FOR proposal #7 on April 29.

Whenever your money moves it has an impact – as an investor, you need to know these 5 things to make the impact of your wealth more fair and sustainable.

Newground filed a shareholder proposal that calls on Goldman Sachs to expand its public disclosure of lobbying expenditures. Lobbying transparency helps shareholders ensure that management behaves in alignment with their interests, and is increasingly considered a best practice on Wall Street.

Jesse Jackson was a visionary who understood, decades before it became mainstream practice, that the boardroom was a battleground for justice just as surely as the courthouse or the ballot box.

While government shutdowns are frustrating, history suggests they are not a reason for long-term investors to panic.

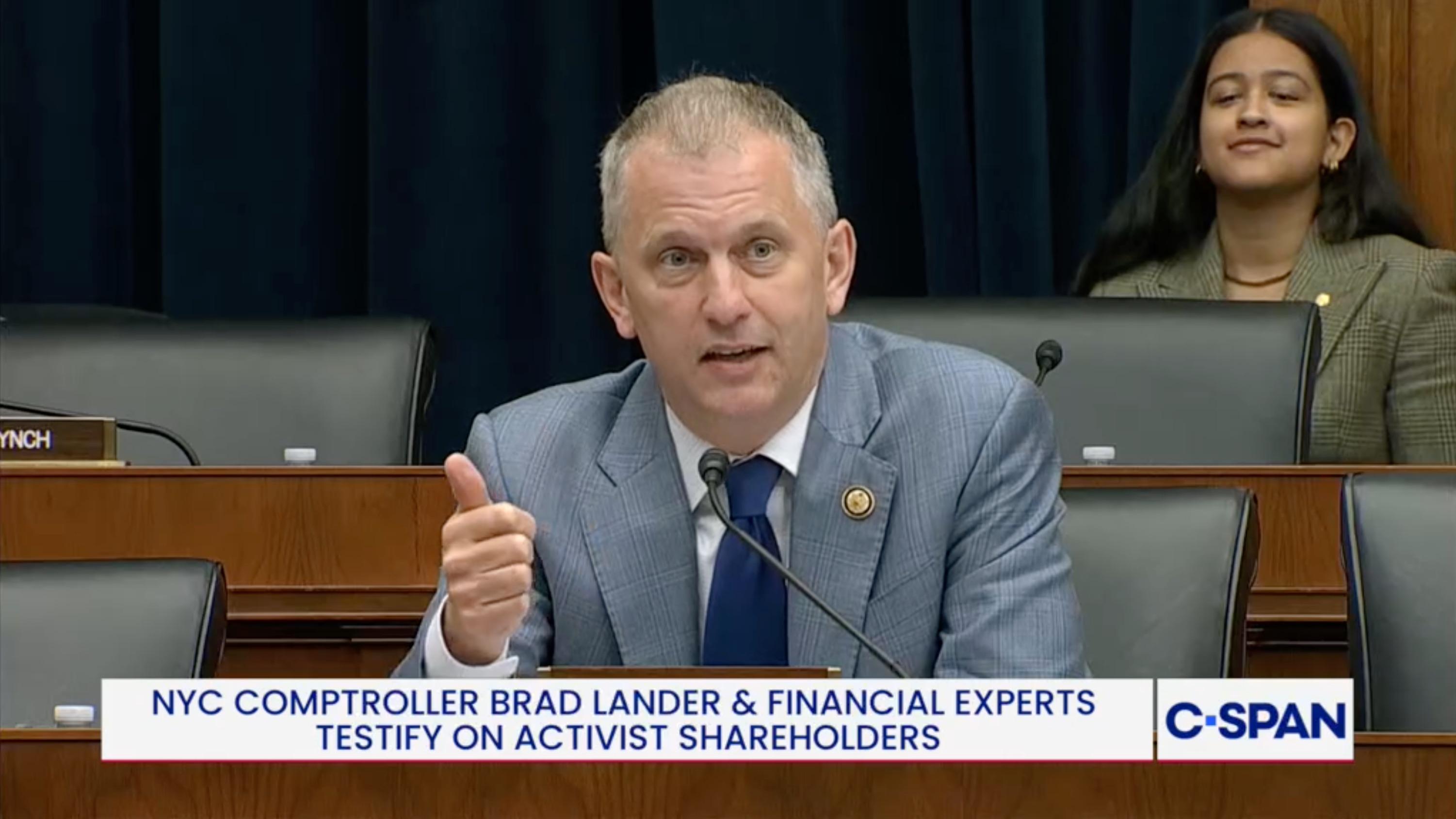

During a fiery House Financial Services Committee Hearing, Rep. Sean Casten (D-IL) offered a masterclass in how to counter right-wing attacks on ESG investing and shareholder democracy.

TESLA is using a new Texas law to silence investors who own less than $1 million in stock. Newground has filed a shareholder proposal challenging the move.

In philanthropy, endings deserve as much care and clarity as beginnings. As more nonprofits decide to sunset and spend down, this best-practices checklist ensures you act with intention, integrity, and impact.

While Capitol Hill races to finalize sweeping changes in the so-called One, Big, Beautiful Bill, much remains unresolved. Read the latest for valuable clues on where tax policy may be headed.

Alec Baldwin speaks at the 2025 Chevron stockholder meeting, to seek greater access & accountability regarding negative environmental & human rights issues caused by the Company.

On this Earth Day, we reflect on the profound guidance of Pope Francis, who said, “To be protectors of God’s handiwork is not an option.”

The most important thing we can do is to take informed action and maintain, as Sir Winston Churchill put it, a spirit of calm determination . . . because setbacks are inevitable, but giving up is unforgivable.

Newground filed a shareholder proposal with Tesla that calls for disclosure of its corporate political spending. Transparency on "dark money" spending would foster trust with shareholders, improve oversight, and protect democracy.

Newground filed a shareholder proposal that calls on Amazon to address misalignment between its public commitments on climate action, versus the company's political and "dark money" lobbying that undermine those commitments.

Washington Post quotes Newground's Bruce Herbert: "In the long run, what’s most profitable is also often most sustainable..." (How to decide whether sustainable investing is right for you. 2024.1211)

To reduce risk and improve oversight related to pollution and human rights abuses, Newground filed a shareholder proposal that calls on Chevron to lower the threshold needed to convene a special meeting of shareholders.

A great question – that many investors wonder about – is whether their account would grow faster if they changed from where they are into a more growth-oriented investment model.

As Gertrude Stein once said: "Silent gratitude isn’t much use to anyone." In light of recent events we are feeling tremendous thanks for the Newground family, therefore we thought it would be useful to not keep silent about it!

History teaches that dark hours have a way of awakening the light in people – often sparking powerful movements of resistance and reform.

As college costs skyrocket, families are turning to friends and relatives for help funding 529 education plans. Here's one service that makes it easy.